Our website has detected that you are using an outdated browser that will prevent you from accessing certain features. An upgrade is recommended to improve you browsing experience.

3

3

Macroprudential Policy (continued)

Although the FSR Act assigns the main legal responsibility for preserving financial stability to the SARB, it also recognises the fact that it is not a mandate that can be achieved by one authority alone. Section 26 of the FSR Act directs that financial sector regulators (i.e. the PA, FSCA, FIC and NCR) must co-operate and collaborate both with the SARB and each other to maintain, protect and enhance domestic financial stability. Financial sector regulators are also obliged to provide such assistance and information to the SARB and FSOC to maintain or restore financial stability as may reasonably be requested, and to promptly report to the SARB any matter of which financial sector regulators become aware that may pose a risk to financial stability.

The SARB, in turn, is mandated to take steps to mitigate risks to financial stability, including advising other financial sector regulators, and any other organs of state, of the steps to take to mitigate those risks. In terms of section 18 of the FSR Act, the Governor may direct a financial sector regulator to assist and provide information to the SARB to (a) prevent systemic events from occurring; and (b) if a systemic event has occurred or is imminent, to mitigate the adverse effects on financial stability and manage the systemic event and its effect.

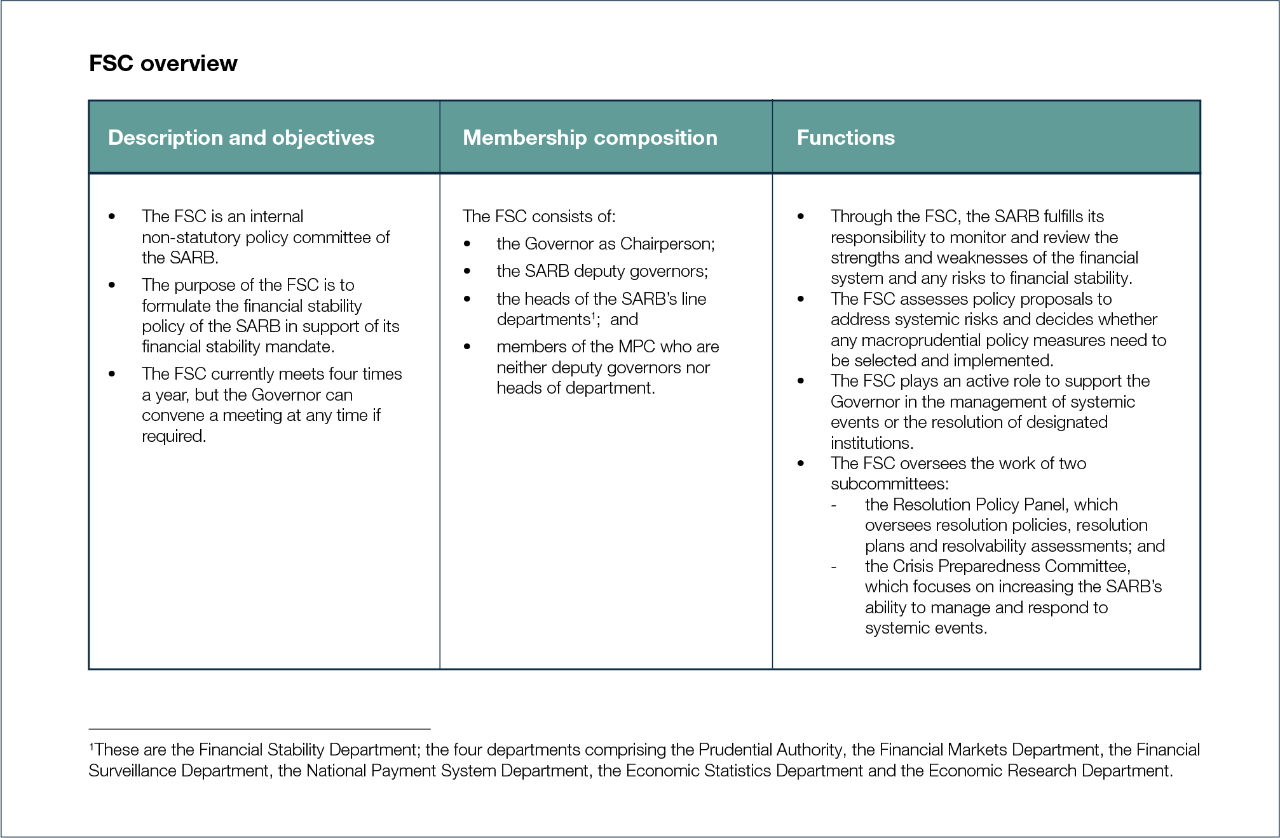

The broad scope of the financial stability mandate requires a high degree of interagency coordination and cooperation. The FSR Act makes provision for such interaction through the establishment of the FSOC. In addition, the SARB has established an internal, non-statutory committee − the Financial Stability Committee (FSC) – to facilitate cooperation among its various line functions in the execution of its financial stability mandate. The composition and functions of the FSC and FSOC are set out in the table below.

Macroprudential policy

Resolution planning

Stress testing

Committee structure

Research

Financial Stability Review (FSR)

Coordination

SARB macroprudential policy framework and decision-making process

SARB financial stability monitoring and assessment framework

Newsroom

Publications

Statistics