Our website has detected that you are using an outdated browser that will prevent you from accessing certain features. An upgrade is recommended to improve you browsing experience.

3

3

The inflation target is set by National Treasury in consultation with the SARB. The SARB then independently makes monetary policy decisions, to achieve the target. Specifically, the SARB’s Monetary Policy Committee decides on a level for the SARB Policy Rate (SPR), a short-term interest rate which affects many other rates in the economy.

The SARB’s mandate, set out in the Constitution, requires it to protect the value of the rand in the interest of balanced and sustainable growth. To give effect to this mandate, the SARB uses an inflation-targeting framework. The inflation target is 3% with a tolerance band of plus or minus 1 percentage point.

Monetary policy is implemented by setting the SPR. This instrument was previously known as the ‘repo rate’, a term adopted when the SARB used a shortage system for policy implementation. During this period the SARB lent liquidity to commercial banks using repurchase (repo) agreements. In 2022, however, the SARB transitioned to a surplus framework, where monetary policy transmission works through a deposit facility rather than a lending facility. Detailed information on this framework is available here.

The SARB publicly announces the policy rate every two months.

South Africa formally introduced inflation targeting in February 2000. This framework allows the central bank to use monetary policy tools, mainly short-term interest rates, to keep inflation within a specific target. For 25 years, South Africa's inflation target range has been 3−6%. In 2025, it was revised to a point target of 3%, plus or minus 1 percentage point.

Before adopting the inflation-targeting framework, the SARB used several different approaches, including exchange rate targeting and money supply targeting. The inflation-targeting approach has proved more successful, enabling a more realistic alignment between the SARB’s tools and objectives. It has also enhanced transparency and accountability by providing the SARB with a clear and publicly visible objective.

Inflation is an increase in the general price level of an economy.

Inflation involves much more than price shocks such as higher petrol prices. Most economies are inflating all the time: every year, prices are generally higher than they were the year before. For instance, in South Africa, consumer prices rose by 65% between 2010 and 2020, at an average annual inflation rate of 5.2%. Other countries had different inflation rates over the same period. For example, inflation in the United States averaged 1.8%; in Turkey it was nearly 10%. This shows that inflation dynamics reflect a country’s economic structures and policy choices.

In South Africa, the standard measure of inflation is Statistics South Africa’s (Stats SA’s) consumer price index. This index represents a typical basket of goods and services used by South African households, comprising everything from lottery tickets and petrol to life insurance. Stats SA monitors these prices throughout the year, and reports any changes each month.

Monetary economists identify three basic causes of inflation: demand, supply and expectations.

These three drivers of inflation interact in complex ways. For example, a rise in fuel prices can increase inflation (supply-side shock). But if workers and firms then change their inflation expectations in response to the fuel price shock, inflation may increase due to expectations.

Inflation is fundamentally a monetary phenomenon. Prices can fluctuate for reasons other than monetary policy, but a sustained change in the price level requires more money in circulation, and therefore the consent of the central bank which prints it.

Printing money is perhaps the most obvious cause of inflation, responsible for all historical hyperinflations. But except for extreme cases, changes in the amount of money in circulation do not predict inflation very well. For this reason, economists now rarely study money supply data to understand inflation, focusing instead on the factors described above.

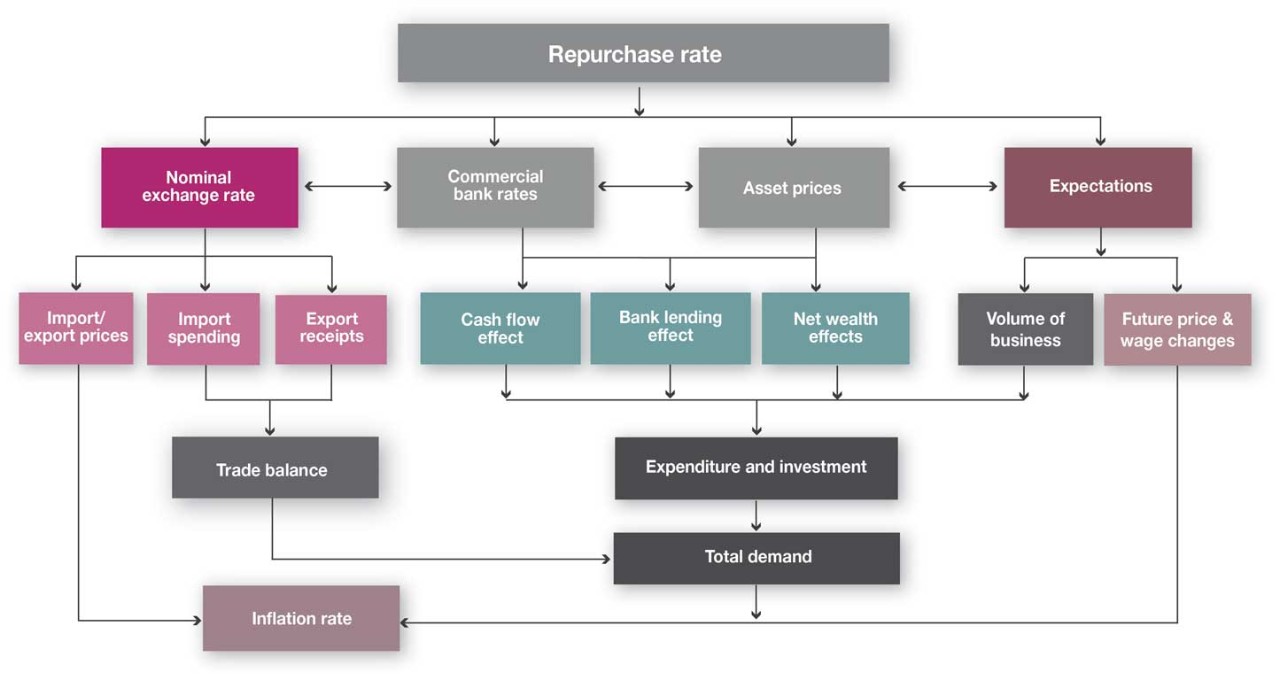

Monetary policy in South Africa aims to achieve and maintain price stability in the interest of balanced and sustainable economic growth and transmits to the economy through different channels.

Consider a scenario where the central bank raises the interest rate. This will do at least four things:

First, it will increase costs for borrowers with floating interest rate debt (such as the interest rate on home loans). It will also promote saving and discourage borrowing. Together, these effects weaken demand, reducing price pressures in the economy. (This is often called the savings and investment channel).

Second, a higher interest rate will tend to strengthen the rand’s exchange rate by improving returns on rand-based investments. In turn, a stronger rand reduces the price of imported goods. (This is the exchange rate channel).

Third, by raising rates, the central bank signals a commitment to reduce inflation. Price and wage setters will factor this expected reduction into their wage and price decisions. (This is the inflation expectations channel).

Fourth, higher interest rates will affect asset markets by, for example, moderating house prices. This can reduce the wealth of asset owners and cause them to reduce their purchases, slowing the economy. (This is known as the wealth channel).

The core idea of inflation targeting is that monetary policy has only temporary effects on growth, but permanent effects on prices.

Inflation targeting grew out of two theoretical breakdowns. In the 1970s, many central banks accepted higher inflation because they believed it would boost economic growth, but instead it resulted in stagnant growth and higher inflation (i.e. stagflation). ‘Monetarist’ approaches, which became influential in the 1980s, also failed, as central banks realised that changes in money supplies were only loosely related to the outcomes people cared about, such as inflation. Inflation targeting provided an elegant solution to the flaws of both these frameworks. A number of countries, such as Brazil and the United Kingdom – and to some extent South Africa – adopted inflation targeting due to the failure of a third policy: managing exchange rates. These policy experiences showed that inflation was more controllable, and more relevant, than other variables central banks had tried to target.

In practice, inflation targeting has demonstrated several other advantages. It has made central banks more accountable, because their performances can now be assessed against clear metrics: their inflation targets. It has also made them more transparent in their communications. When the public understands what monetary policy is trying to achieve, and trusts the central bank to deliver, success is more likely.

Furthermore, although inflation targeting was built on the premise that monetary policy cannot permanently affect ‘real’ variables such as growth and employment, the framework has allowed policymakers to respond better to cyclical fluctuations in economic performance. Credible monetary policy stabilises inflation, allowing central banks to lower rates during periods of economic weakness. The claim that inflation-targeting central banks ignore growth is therefore incorrect.

South Africa’s inflation target is 3%, with a tolerance band of plus or minus 1 percentage point.

This target refers to the headline change in the consumer price index, as calculated by Statistics South Africa. The target is determined by the Minister of Finance in agreement with the Governor of the SARB.

Tolerance band: The tolerance band, which allows for 1 percentage point either side of 3%, does not mean the SARB is indifferent to inflation anywhere between 2% and 4%. The goal remains to be at 3%. However, no central bank can deliver inflation at an exact point at all times. Attempting to offset every price shock would also create undesirable volatility in output and the tolerance band helps communicate the flexibility of the framework. Temporary deviations from the target are acceptable, provided that inflation returns to the target range once shocks have passed.

Forward-looking: Policymakers are not required to make up for missing the target in the past, but they are expected to ensure that inflation returns to the target. Policy changes are transmitted over roughly 12 to 24 months and the SARB sets policy to guide inflation back to target over that time horizon.

The Monetary Policy Committee (MPC) meets six times a year to set the repo rate.

The MPC consists of up to seven members, including the Governor of the SARB, the three deputy governors and senior officials appointed by the Governor.

A typical meeting opens with presentations by senior officials covering developments in the global and domestic economy and financial markets, as well as the economic outlook. The staff economists then leave and the MPC members decide on the repo stance and prepare a statement. Finally, the Governor delivers this statement at a televised press conference, which includes a question-and-answer session with journalists.

CURRENT SARB POLICY RATE

CURRENT INFLATION RATE

NOMINAL EFFECTIVE EXCHANGE RATE

Monetary policy committee

Monetary policy implementation

23 September 2026

19 November 2026

Newsroom

Publications

Statistics

Monetary Policy Forums

If you have further questions about monetary policy, please do not hesitate to contact us.