Our website has detected that you are using an outdated browser that will prevent you from accessing certain features. An upgrade is recommended to improve you browsing experience.

3

3

Reserves Management and Foreign Exchange Operations

The SARB’s Gold and Foreign Exchange Reserves Management Investment Policy governs the management of reserves. Reserves are managed within the SARB’s overall risk tolerance framework, and the related strategic benchmarks and targets are encapsulated in Strategic Asset Allocation. A three-tier governance structure clearly segregates the responsibilities for executive authority (Governors’ Executive Committee), strategic management (Reserves Management Committee) and portfolio management (Financial Markets Department). External fund managers manage a portion of the foreign exchange reserves to enhance the internal reserves management capabilities and diversify risk and return.

The SARB has managed and held gold reserves since 1925 and purchased nearly all the locally produced gold. This involvement with gold has, of course, evolved. Currently, the SARB’s activities in gold are much more akin (by design) to those of other central banks.

Following the announcement by the Minister of Finance on 12 December 1997, South African gold producers could elect to sell all of their output themselves to approved counterparties. This dispensation was granted provided that the SARB (on behalf of the Minister of Finance) gave the necessary exemption from the provisions of the Exchange Control Regulations.

Statement of Commitment to the Global Precious Metals Code

The South African Reserve Bank (SARB) has reviewed the content of the Precious Metals Global Code (Code) and acknowledges that the Code represents a set of principles generally recognised as good practice in the wholesale precious metals market (market). The SARB confirms that it acts as a market participant as defined by the Code, and is committed to conducting its market activities (activities) in a manner consistent with the principles of the Code. To this end, the SARB has taken appropriate steps, based on the size and complexity of its activities, and the nature of its engagement in the market, to align its activities with the principles of the Code.

Date: 1 February 2026

Official gold and foreign exchange reserves management investment policy

The Investment Policy provides a strategic framework that guides the Financial Markets Department and the Reserves Management Committee in their respective roles in the reserves management process. The Investment Policy specifies, among other things, the aggregate tolerance parameters of the SARB and the eligible asset classes, which are implemented through Strategic Asset Allocation.

Capital preservation

Safety of the principal amount invested is the foremost investment objective. Investments shall be undertaken in a manner that seeks to preserve the capital value of the overall portfolio over the investment horizon, subject to the approved risk tolerances.

Liquidity

Investment management shall seek to ensure that adequate reserves are available to meet a defined range of objectives. In order to maintain sufficient liquidity, reserves shall be invested mostly in securities with an active secondary market.

Returns

Subject to capital preservation and liquidity constraints, the reserves shall be invested with the objective of achieving a reasonable return which is consistent with the investment objectives and risk constraints.

Each of these objectives has specific liquidity requirements and investment horizons. Consequently, the reserves are segregated operationally into sub-portfolios, known as tranches, for investment management purposes.

Strategic Asset Allocation is a quantification of the risk tolerance embedded in the Investment Policy. It is presented as a set of benchmark portfolios weighted to primarily ensure capital preservation, but also to optimise the return profile of the reserves, avoiding downside risks.

Strategic Asset Allocation determines the optimal asset allocation while recognising the risk tolerance and liquidity constraints of the SARB. It sets the tranche sizes, currency composition and appropriate asset classes, and calculates the expected risk and return over the relevant time horizon. These parameters are specified at tranche level. Hence, each tranche has its own asset mix aimed at achieving the investment objectives of the tranche.

The reserves are divided into two tranches, namely the Liquidity Tranche and the Investment Tranche. The Liquidity Tranche size is determined by an adequate level of reserves. Amounts in excess of this are allocated to the Investment Tranche.

The Liquidity Tranche is invested in highly liquid securities to ensure the timely availability and capital preservation of reserves. It is subdivided into four sub-tranches, namely the Special Drawing Rights (SDR) Sub-tranche, the Gold Sub-tranche, the Working Capital Sub-tranche and the Buffer Sub-tranche.

The SDR Sub-tranche focuses on the unique needs of the SARB in respect of South Africa’s membership of the International Monetary Fund (IMF). SDRs can be exchanged for currencies of the IMF member countries during crises and, as such, are viewed as insurance against unforeseen events.

The Gold Sub-tranche is a function of South Africa’s willingness to hold gold as a special reserve instrument. Given gold’s high liquidity, its diversification benefits and its role as a form of currency, it is used as insurance against adverse economic outcomes.

The Working Capital Sub-tranche provides liquidity for short-term liabilities and cash management needs.

The Buffer Sub-tranche caters for unforeseen liquidity needs and serves to replenish the Working Capital Sub-tranche when required.

The Investment Tranche aims to enhance the returns on the reserves portfolio and to cover longer-term contingencies consistent with South Africa’s overall macroeconomic and financial stability policies. It is invested in higher-yielding securities to enhance the return of the portfolio while recognising the capital preservation and liquidity objectives.

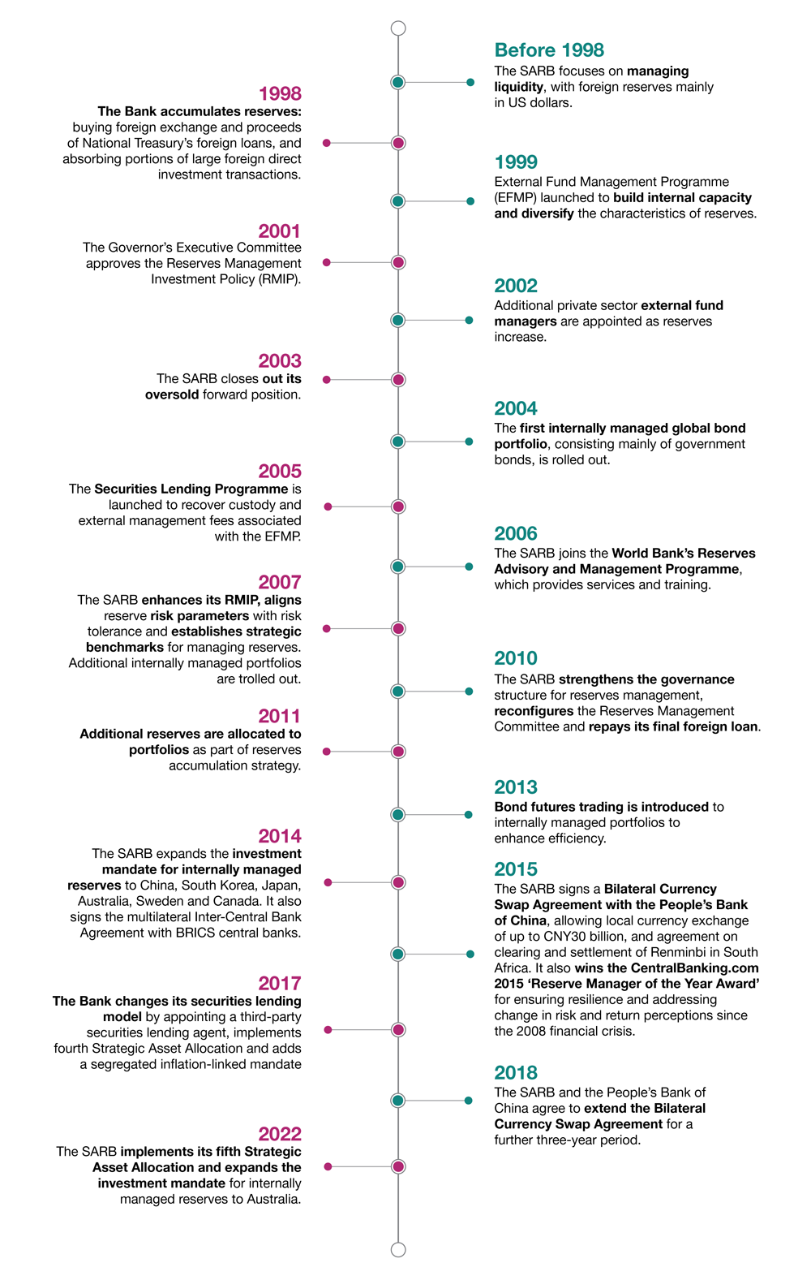

The SARB, similar to other central banks, complements its internal reserves management activities with a well-structured external fund management programme. The rationale for this programme is mainly to enhance and build internal capacity and diversify the risk/return characteristics of the reserves.

The programme, which was introduced in 1999, is periodically reviewed and refined to best suit the requirements of the SARB – in particular, the strategic asset allocation of its reserves. The skills and knowledge transfer initiatives, which the SARB’s staff members have greatly benefitted from over the years, have allowed them to manage more complex portfolios. However, over time the SARB’s external fund management objectives have changed and they now focus on diversification. The SARB therefore allows external fund managers, given their higher level of professional expertise, more leeway in terms of risk-taking and the asset classes they can invest in.

To ensure that the SARB’s funds remain relatively safe during the external fund management tenure, a rigorous legal process is followed in drafting the Investment Management Agreements and Investment Guidelines. In addition, formal portfolio performance reviews are presented on-site to the SARB’s Reserves Management Committee.

Good governance and sound functional organisational structures are essential for the efficient management of domestic operations and reserves management. In establishing these structures, accountabilities, roles and responsibilities should be appropriately defined, adopted and institutionalised.

The Bank’s Board, the Board Risk and Ethics Committee (BREC), the Governors’ Executive Committee (GEC), the Risk Management Committee (RMC), and the Reserves Management Committee (Resmanco) provide independent risk control and compliance functions, supported by the relevant functional departments. The Bank’s Board is responsible for the oversight of the entire process of risk management.

South Africa adheres to a floating exchange rate policy, where the nominal exchange rate is determined by market forces. However, the SARB is not indifferent to challenges posed by volatility and abrupt adjustments of the exchange rate

The Bank may get involved in the foreign exchange market to smooth out abrupt and severe adjustments of the exchange rate, to facilitate an orderly functioning of the foreign exchange market, as well as for financial stability reasons.

In implementing its foreign exchange operations, the SARB mainly conducts spot purchases to accumulate reserves and to service clients’ foreign exchange needs, while foreign exchange swaps are used to manage domestic money market liquidity. Gold and foreign exchange reserves (customarily denominated in the major currencies) are the official public sector foreign assets that are readily available and typically held to:

Maintaining an adequate level of reserves boosts investor confidence, thereby helping to reduce the likelihood of capital outflows.

Foreign exchange reserves are accumulated through open market purchases, when market conditions allow, that is, without unduly influencing the exchange rate or adding to volatility in the market. In exceptional circumstances, the SARB directly purchases a portion of foreign direct investment inflows, flows related to mergers and acquisitions, and proceeds from government foreign currency issues.

Financial markets

Monetary policy implementation framework

Risk management and compliance

Committees and working groups

Gold coins purchased from the public

Market practioners group

Monetary Policy

Latest news and information

Current market rates

Financial markets factsheets

Auctions calendar

Information notices

If you have further questions about the management of official foreign-exchange reserves, please do not hesitate to contact us.