Our website has detected that you are using an outdated browser that will prevent you from accessing certain features. An upgrade is recommended to improve you browsing experience.

3

3

The purpose of prudential regulation and supervision is to ensure that financial institutions and market infrastructures operating within the financial system are inherently safe and sound.

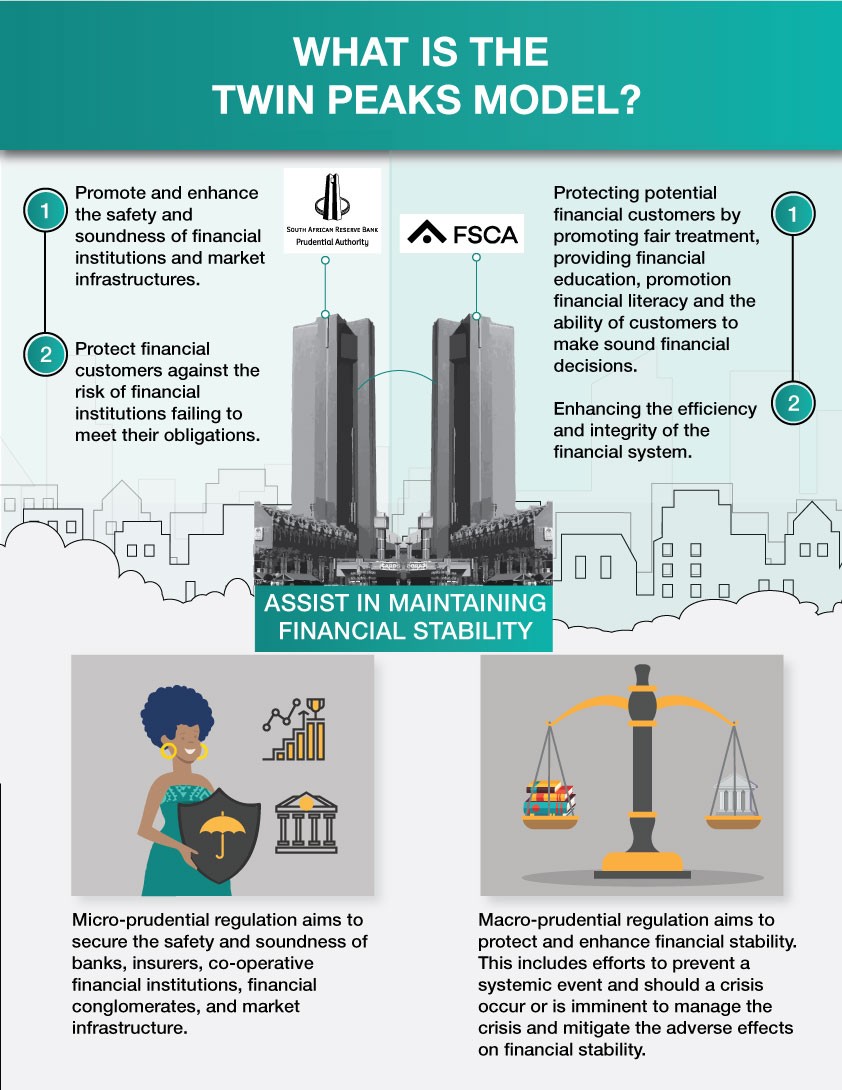

In June 2011, Cabinet approved the move towards the Twin Peaks model. The Twin Peaks model for financial sector regulation was proposed as a means to reform the regulatory and supervisory system for financial institutions and market infrastructures.

The Financial Sector Regulation (FSR) Act was signed into law on 21 August 2017, marking an important milestone on the journey towards a safer and fairer financial system that is able to serve all citizens.

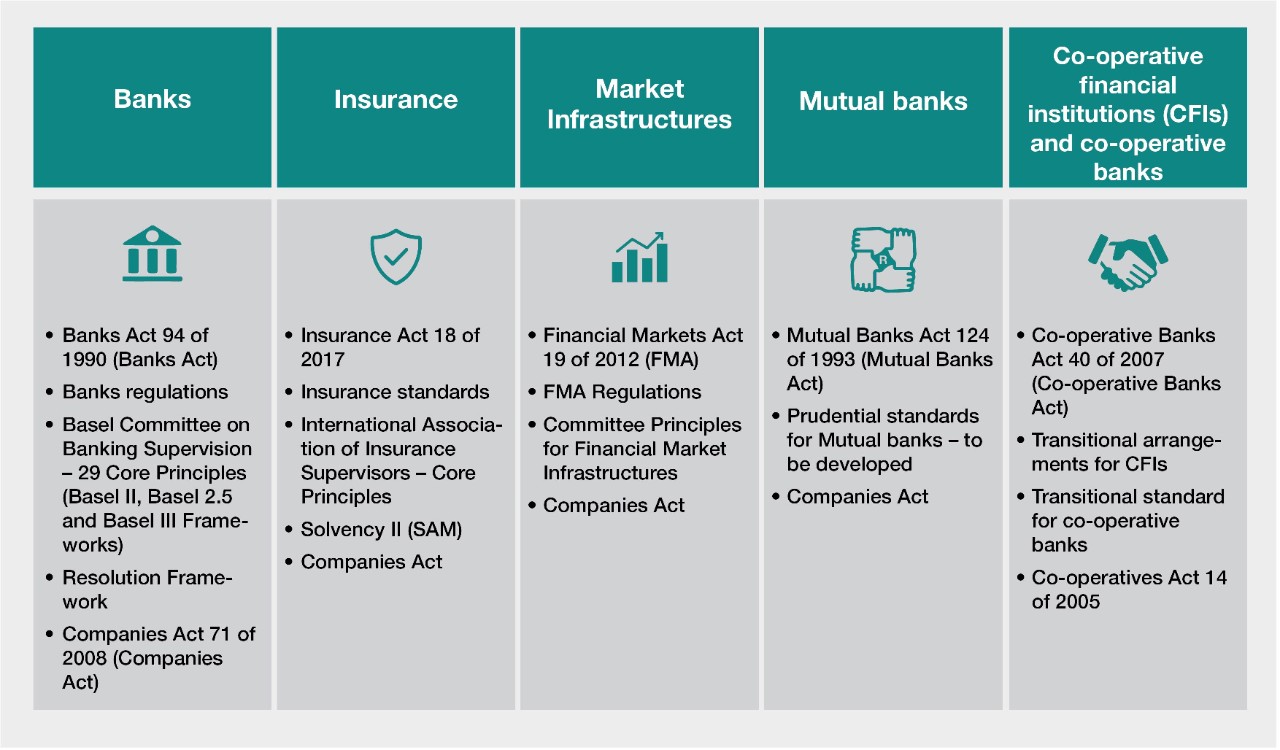

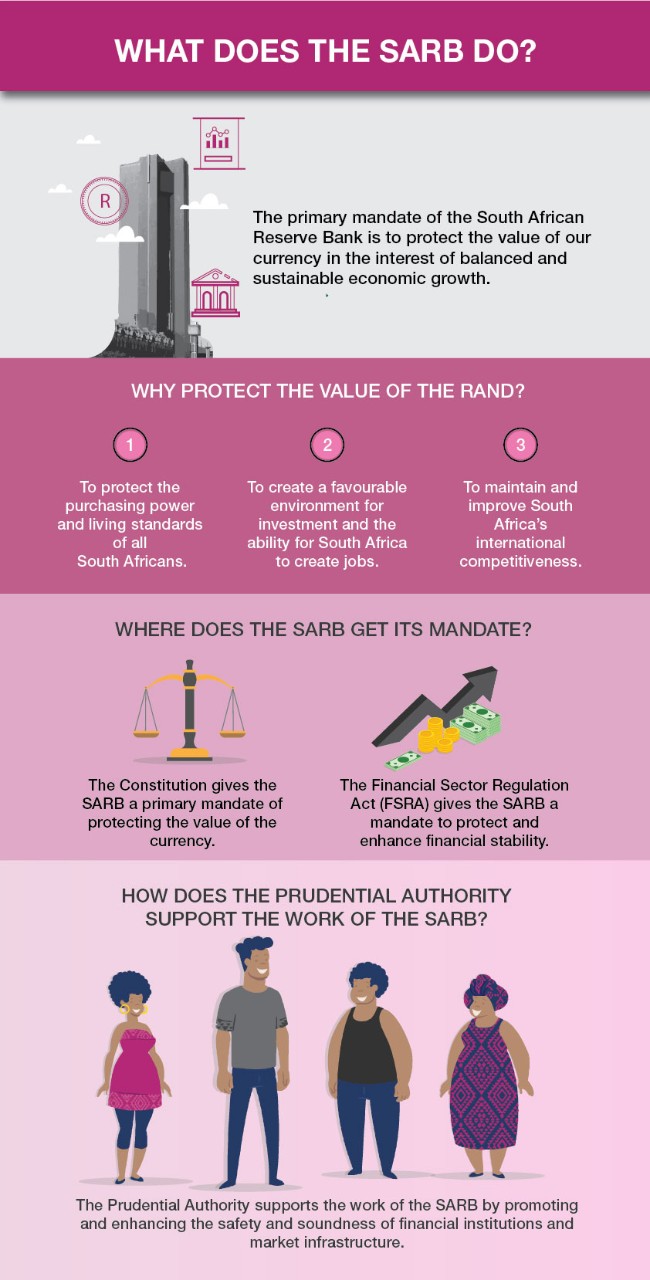

The FSR Act gives effect to three important changes to the regulation of the financial sector. Firstly, it gives the SARB an explicit mandate to maintain and enhance financial stability. Secondly, it creates a prudential regulator – the Prudential Authority (PA) – within the administration of the SARB. The PA is responsible for regulating banks (commercial, mutual and co-operative banks), insurers, co-operative financial institutions, financial conglomerates and certain market infrastructures. Thirdly, the FSR Act establishes a market conduct regulator – the Financial Sector Conduct Authority (FSCA) – which is a national public entity.

The transition to the Twin Peaks model of regulation is being implemented in phases. The first phase was to establish the respective regulatory authorities – the PA and FSCA. The second phase entails developing, harmonising and strengthening the legal frameworks for prudential and market conduct regulation and supervision.

As required by the FSR Act, the Prudential Committee of the PA adopted a regulatory strategy to provide general guidance to the PA in performing its regulatory and supervisory functions and achieving its objectives. This regulatory strategy provides information to market participants and the public regarding the PA’s approach to regulation and supervision, the principles that will guide its regulatory and supervisory decisions, its key priorities over a three-year period, and the key outcomes it intends to achieve in order to realise its priorities.

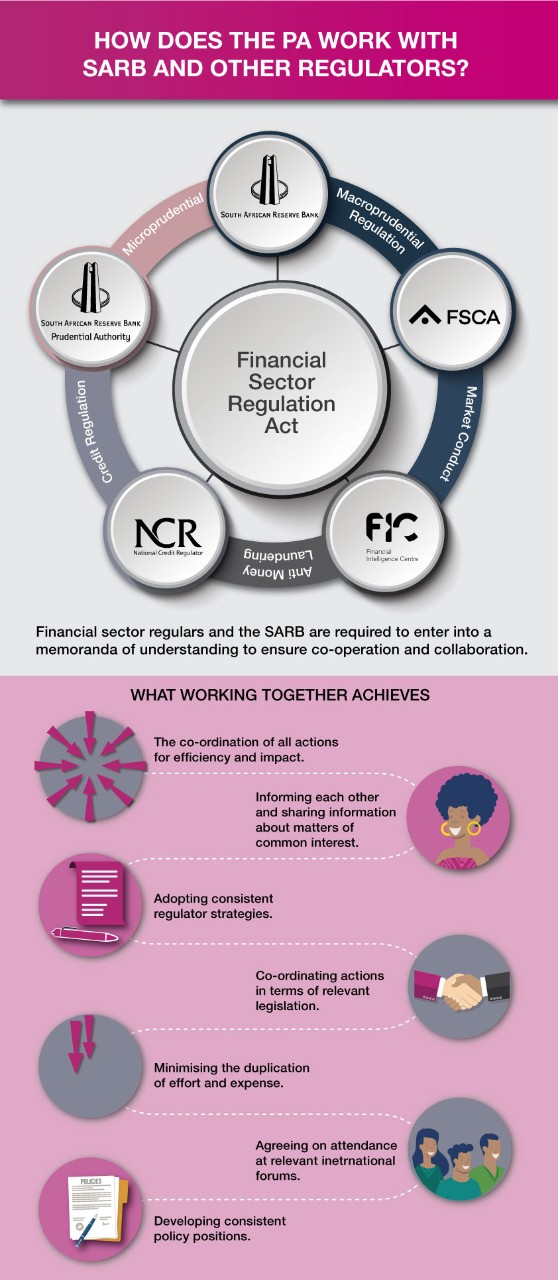

The PA has adopted a collaborative and consultative approach to regulation and engages with other regulators, industry bodies and stakeholders within and outside the financial sector.

Prudential Authority Regulatory Strategy 2018 - 2021

Prudential Authority Regulatory Strategy 2021 - 2024

Prudential Authority Regulatory Strategy 2025 - 2030

A stable financial system is one that efficiently manages the flow of funds through its financial intermediaries, markets and market infrastructures such that it promotes growth in its economic activities.

The term ‘microprudential’ denotes the regulation or supervision of individual financial institutions by the PA. On the other hand, ‘macroprudential’ oversight refers to the responsibilities of the SARB, which is charged with identifying, assessing and mitigating risks for the financial system as a whole.

The financial system plays a critical role in supporting economic activity. Households and businesses need ways to save and borrow in order to fund consumption and investment; payment systems to facilitate local and international transactions; and insurance to manage their day-to-day risks. The public needs to be confident that banks, non-bank deposit takers and insurers can and will continue to provide these services, and that the payment and settlement systems will work as expected.

However, the financial system is exposed to risks, which come from a wide range of sources, both global and domestic. The South African financial system is also relatively small and open, and is dominated by a handful of institutions that are highly connected. The distress or failure of one of the major institutions is likely to have significant implications for the system as a whole.

With effect from 1 April 2018, when the PA was established, the Bank Supervision Department of the SARB ceased to exist. The resultant PA consists of the following four departments: the Financial Conglomerate Supervision Department; the Banking, Insurance and Financial Market Infrastructures Supervision Department; the Risk Support Department; and the Policy, Statistics and Industry Support Department.

In fulfilling its mandate to promote and enhance the safety and soundness of financial institutions, the PA is responsible for:

The PA is a juristic person operating within the administration of the SARB. It is not a public entity in terms of the Public Finance Management Act 1 of 1999. The PA is headed by a chief executive officer (CEO) who must be a deputy governor of the SARB but not the deputy governor responsible for financial stability. The CEO’s term of office is five years and the CEO is eligible for reappointment for one further term. The PA is governed by the Prudential Committee, which consists of the governor of the SARB, the CEO of the PA, and the deputy governors of the SARB. The Prudential Committee is mandated to oversee the management and administration of the PA to ensure that it is efficient and effective.

While, in general, South Africa has a modern and prudent financial sector that protects the interests of all customers and citizens, there are too many cases of abuse and exploitation in the sector and the sector still poses immense risks to the economy. Effective regulation will help make the financial sector more responsive to the needs of all South Africans.

Sector Data

Documents Issued for Consultation

FSCA

Legislation and regulatory instruments

National Treasury

Public awareness

South African registered financial institutions

PA Designated Entities

PA Transformation Programme

Legislation

If you have further questions about prudential regulation, please do not hesitate to contact us.